If you walk into most African universities, everything looks normal.

Students laughing. Lecturers talking. Assignments being submitted five minutes before the deadline – as tradition demands.

From the outside, it looks like a system working.

But spend five minutes inside a student’s head, and you’ll realise something is off.

Because beneath all that laughter, there’s pressure. Not the loud, obvious kind – the kind that screams deadlines and exams. No, this one is quieter. It sits in the background. It follows you to class, eats with you, studies with you, and sleeps next to your unfinished assignments.

It’s the kind of pressure that doesn’t announce itself. It just exists.

And the problem with silent pressure is simple: if nobody talks about it, everyone thinks they’re the only one feeling it.

In many parts of the world, going to university is an option. In Africa, for many families, it’s a mission. You are not just a student – you are hope. And hope is heavy.

1. The Pressure to Just “Make It”

In many parts of the world, going to university is an option. In Africa, for many families, it’s a mission. You’re not just going to school – you’re carrying expectations. Generations of them. You are the investment.

Somewhere back home, there’s a parent who didn’t get this chance. Or a sibling who sacrificed their own opportunity so you could sit in that lecture hall. Or a community that contributed money, advice, prayers – sometimes all three.

So when you step into university, you’re not just Assan, or Fatou, or Kwame. You are hope. And hope is heavy.

Because failing an exam doesn’t feel like failing a course – it feels like disappointing an entire village. Nobody says it out loud, of course. Africans are very polite when it comes to pressure. Instead of saying, “Don’t fail us,” they say things like: “We’re proud of you.” Which sounds supportive… until you realise it comes with an invisible contract: stay worthy of that pride.

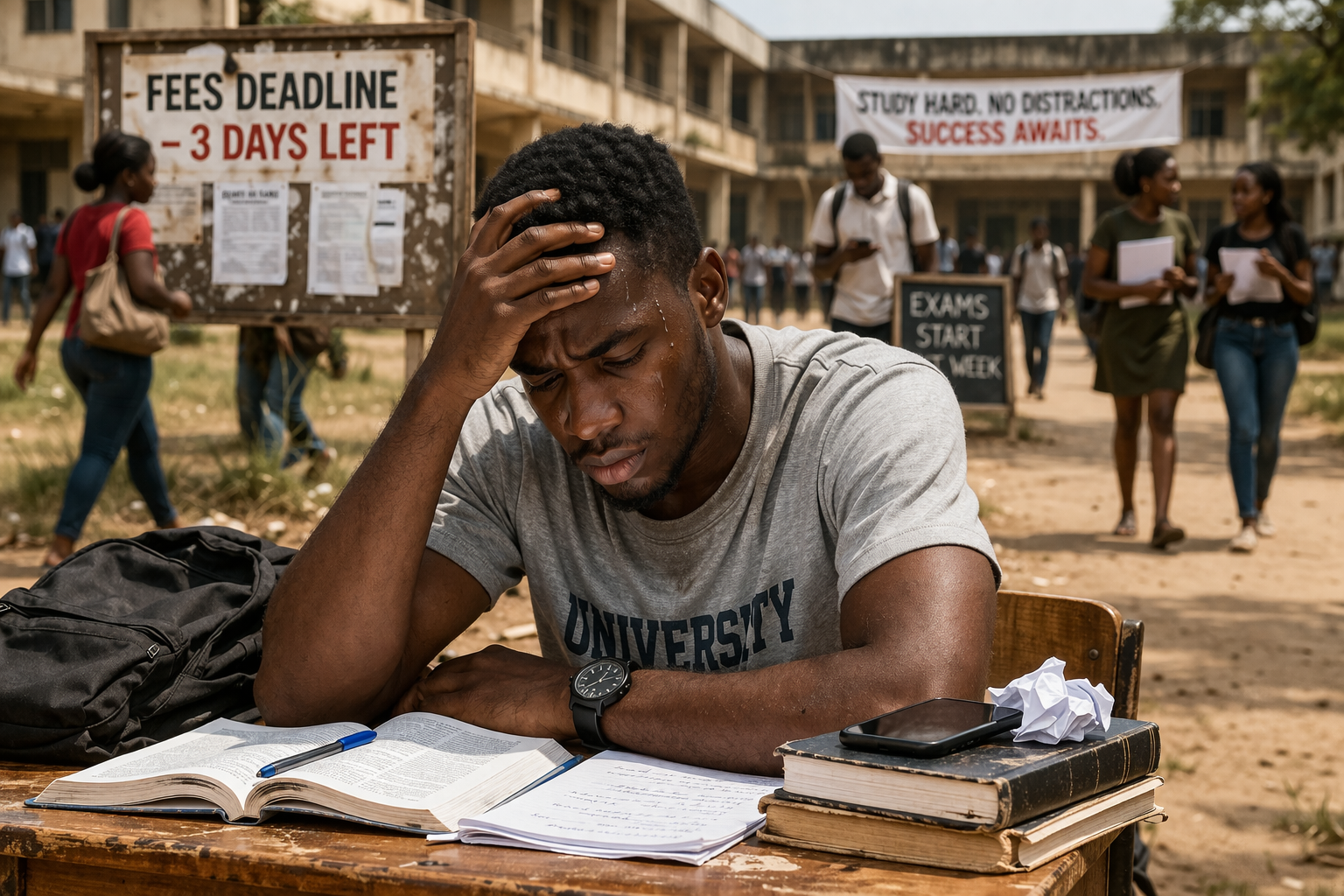

2. The Financial Pressure Nobody Wants to Admit

Let’s talk about money. Actually – let’s talk about the lack of it. Because being a student in many African universities often means living in a constant balancing act between needs and reality.

You calculate everything: Can I afford this meal? Should I print this assignment or just submit it digitally and hope the lecturer understands? Do I buy data for studying… or save it for communication?

And here’s the part nobody says out loud: sometimes, education starts to feel like a luxury you can’t fully afford. Not just tuition – everything around it. Books. Internet. Transportation. Food.

So you start making compromises. You skip meals. You delay purchases. You stretch resources in ways that would impress even the most disciplined economists. And yet, despite all this, you’re expected to perform at the same level as someone who doesn’t have to think twice about any of these things. That’s not just pressure. That’s pressure with interest.

Most students are carrying a silent financial weight – and still showing up to class, still submitting assignments, still trying to compete. That is not weakness. That is resilience.

3. The Comparison Game (That Nobody Wins)

University is supposed to be about learning. Instead, it often becomes a competition you didn’t sign up for. You see classmates getting internships, starting businesses, posting achievements online, “winning” at life before graduation. And suddenly, your own journey feels… slow.

It doesn’t matter that everyone’s path is different. Logic disappears when comparison enters the room. Because now you’re asking questions like: “What am I doing wrong?” “Why am I behind?” “Am I wasting my time?”

And social media makes it worse. Because nobody posts their struggles. You’ll never see someone say: “Failed my exam today. Confidence at zero. Thinking of restarting life.” No. You’ll see: “Grateful for this journey. Big things coming.” Meanwhile, their reality looks exactly like yours. But because nobody admits it, everyone feels alone.

4. The Pressure to Choose the “Right” Course

In theory, you choose your degree. In reality… it’s complicated. Sometimes you pick a course because it sounds prestigious, your parents suggested it, society respects it, or you didn’t know what else to pick. So you end up studying something that looks good on paper… but feels wrong in your gut.

And now you’re stuck. Because changing courses isn’t always easy. And quitting? That’s not even an option. Not after everything that’s been invested in you. So you stay. You attend lectures that don’t excite you. You study topics that don’t inspire you. You chase grades in something you’re not even sure you want. That’s not education. That’s survival with a syllabus.

5. The Unspoken Fear of the Future

Here’s the truth nobody wants to say during orientation week: a degree does not guarantee a job. Students know this. They see graduates struggling. They hear stories. They watch people finish university and then… pause.

And that creates a quiet fear. Because now, every lecture comes with a question: “Will this actually help me later?” Every assignment feels like: “Am I preparing for something real… or just passing time?” And the closer you get to graduation, the louder that fear becomes. It’s like standing at the edge of a cliff, knowing you have to jump – but nobody told you what’s at the bottom.

“Most students are carrying the same weight. They’re just carrying it quietly.”

6. The Pressure to Appear Strong

Here’s where it gets dangerous. In many African cultures, strength is expected. You don’t complain too much. You don’t show weakness easily. You “handle it.” So when things get overwhelming, you don’t talk about it. You smile. You joke. You say, “I’m fine.” Even when you’re not.

Because admitting struggle feels like failure. And failure? That’s not part of the script. So people suffer quietly. Not because they want to – but because they don’t feel like they have permission not to.

7. The Double Life Students Live

There’s your university life. And then there’s your real life. In university: you’re learning, socialising, building a future. Outside: you might be supporting family, working part‑time, dealing with personal challenges nobody knows about.

The hardest part? Switching between the two. Imagine sitting in a lecture about theoretical concepts… while your mind is thinking about real‑life problems waiting for you after class. That’s not distraction. That’s divided existence.

8. The Migration Dream

Let’s address the elephant in the room. For many students, university is not the destination. It’s a stepping stone to somewhere else. The dream of leaving – of finding better opportunities abroad – is always there. Sometimes it’s subtle. Sometimes it’s the main goal.

And that creates another layer of pressure. Because now, your degree isn’t just about success – it’s about escape. You’re not just studying to graduate. You’re studying to unlock a door. And when that door feels uncertain, everything else starts to feel uncertain too.

Everyone struggles alone. And when people struggle alone, they start to believe things that aren’t true: “I’m the only one feeling this way.” “Everyone else has it figured out.” “Maybe I’m just not good enough.” The reality is: most students are carrying the same weight – just quietly.

9. The Truth (That Changes Everything)

Here’s the part where we stop pretending. The pressure is real. It’s not imagined. It’s not exaggerated. It’s not a sign of weakness. But here’s what is dangerous: letting that pressure define you. Because pressure can either crush you or shape you. And the difference isn’t the pressure itself – it’s how you respond to it.

Final Thought

If there’s one thing worth understanding, it’s this: you were never meant to carry all of this perfectly. Not the expectations. Not the financial stress. Not the uncertainty. The system is tough. The environment is demanding. But that doesn’t mean you’re failing. It might just mean you’re navigating something that was never designed to be easy.

And maybe – just maybe – the strongest thing you can do isn’t pretending everything is fine. It’s recognising the weight… and still choosing to move forward anyway. Not perfectly. But honestly.